{kind=link}

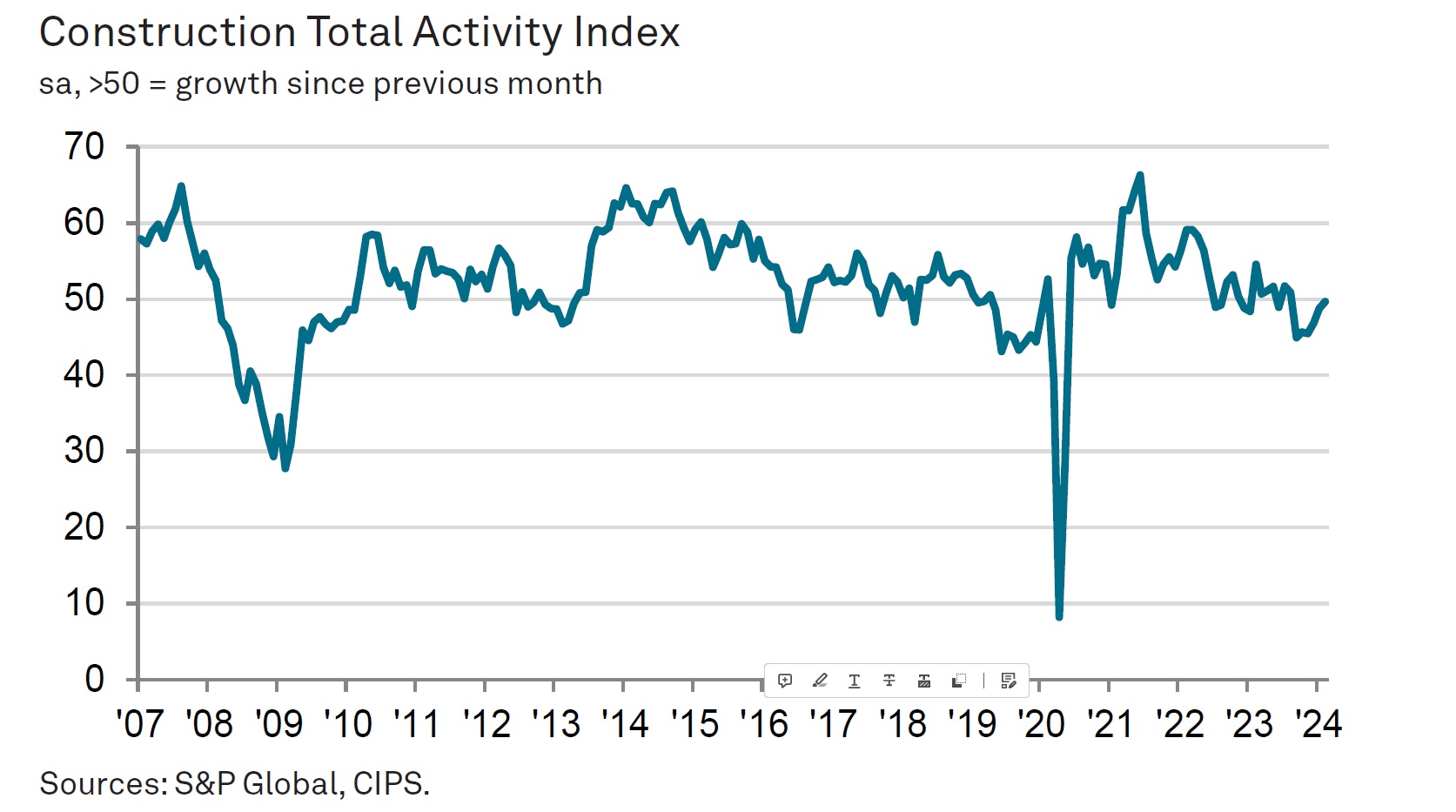

The heading S&P Global UK Construction Purchasing Managers’ Index (PMI) stays in unfavorable development area, at 49.7 for February (up from 48.8 in January), however only simply listed below the 50.0 no-change mark and its greatest level because August 2023.

Just limited, the rate of brand-new service development was the fastest because May 2023 and company optimism enhanced for the 3rd time in the previous 4 months to reach its greatest level given that January 2022.

The rate of task shedding was the fastest considering that November 2020.

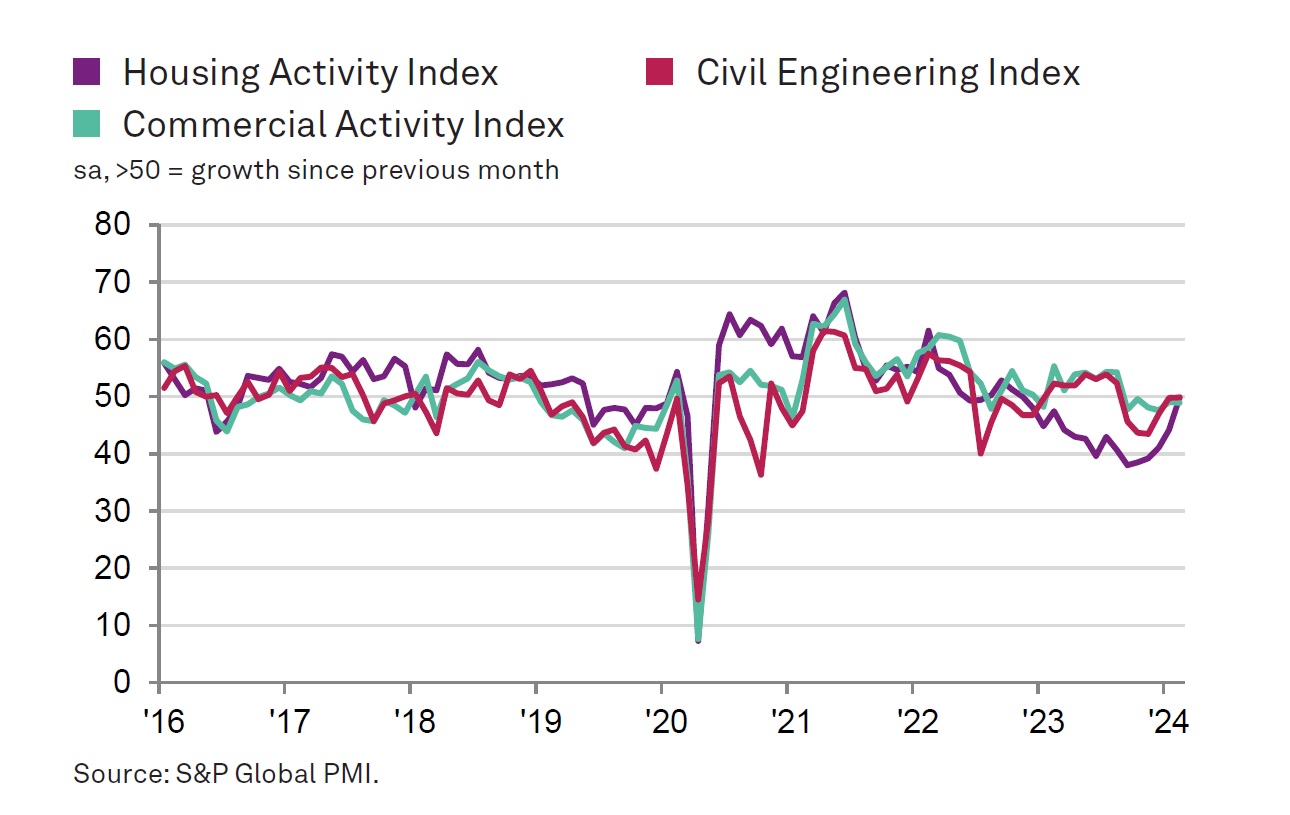

All 3 primary classifications of building and construction activity saw a near-stabilisation of company activity in February. House-building saw the most significant turn-around because January, with its index at 49.8, up from 44.2 and its greatest level considering that November 2022. Study participants recommended that enhancing market conditions had actually slowly added to a stabilisation of property building and construction work. On the other hand, the business sector saw a more controlled efficiency than in January, with building business normally mentioning hesitancy amongst customers and constrained budget plan setting.

Overall brand-new work increased partially in February, ending a six-month duration of decrease. This appeared to show a turn-around in tender chances and higher customer self-confidence, specifically in house-building.

Regardless of favorable patterns for order books and sales pipelines, staffing numbers reduced for the 2nd month running and, although just moderate, the rate of task shedding was the fastest given that November 2020. Remarks from panel members recommended that a current soft spot for deal with website, together with strong wage pressures, had actually resulted in cost cutting steps consisting of the non-replacement of voluntary leavers.

Majority of the study panel (51%) expect an increase in organization activity throughout the years ahead, while just 6% anticipated a decrease. This shows the greatest degree of organization optimism for simply over 2 years. Building and construction business primarily kept in mind brand-new task starts and favorable signals for client need, partially connected to anticipated rates of interest cuts.

Supply conditions on the other hand enhanced once again somewhat in February. There were some reports of an unfavorable effect on shipments of building items due to Red Sea shipping disturbances. Need for building and construction inputs stayed reasonably suppressed, as indicated by a decrease in buying activity for the 6th month running.

Typical expense problems increased for the 2nd successive month in February. Greater input rates were frequently connected to strong wage pressures and increasing transport expenses. The rate of inflation was just modest and relieved from January’s eight-month high, with some companies pointing out chances to work out rate discount rates amidst extreme provider competitors.

{kind=link}

Tim Moore, economics director at S&P Global Market Intelligence, which puts together the study, stated: “A stabilisation in home structure implied that UK building output was practically the same in February. This was the very best efficiency for the building and construction sector considering that August 2023 and the positive study signs offer support that company conditions might enhance in the coming months.

“Total brand-new orders broadened for the very first time considering that July 2023, which building and construction business credited to increasing customer self-confidence and indications of a turn-around in the property structure section. The degree of optimism relating to year ahead company activity potential customers was the greatest considering that the start of 2022, in part due to looser monetary conditions and anticipated interest rate cuts.

“However, a lengthy decline in activity has actually made building business mindful about their work numbers. Staffing levels dropped for the 3rd time in the previous 4 months and the current round of task shedding was the steepest given that November 2020. Getting activity likewise reduced in February, however building companies continued to mention supply side difficulties. Input expenses increased for the 2nd month running as strong wage pressures and restored products cost inflation positioned upward pressure on operating expenditures.”

{kind=link}

Brian Smith, head of expense management and business at Aecom, stated:”The return of spring has actually brought a brighter outlook for the sector after a prolonged duration of problem, stemming back 12 months, however it will be forgiven for working out care. Companies have actually succeeded to weather the storm of high inflation and tightening up monetary conditions however, while order books are favorable for this year, the study suggests a more competitive tender market ahead.

“Two-stage contracting is ending up being the favored technique amongst tier one professionals, supplying a chance for two-way early-stage discussions with designers. In spite of a small uptick, the general volume of work readily available will still raise issues for sub-contractors with much shorter pipelines and weaker balance sheets.”

Got a story? Email news@theconstructionindex.co.uk